SIF vs MF vs PMS vs AIF — Which Investment Option is Right for You in 2025?

India’s investment landscape offers multiple ways to grow your wealth — from SIFs (Systematic Investment Funds) and Mutual Funds (MFs) to Portfolio Management Services (PMS) and Alternative Investment Funds (AIFs).

While Mutual Funds are ideal for retail investors seeking diversification and liquidity, PMS offers personalized portfolio management for high-net-worth individuals. AIFs, on the other hand, are designed for sophisticated investors looking for higher returns through private equity, venture capital, or hedge fund-style strategies. SIFs bridge the gap by providing systematic, professionally managed exposure with flexible entry points.

In this detailed comparison, we’ll break down how these four investment types differ in terms of minimum investment, returns, risk level, and tax treatment — helping you decide which one aligns best with your financial goals and risk appetite.

What is SIF (Systematic Investment Fund)?

A Systematic Investment Fund (SIF) is a relatively new investment structure designed to combine the discipline of mutual funds with the flexibility and customization of portfolio management services. Unlike traditional mutual funds, which pool money from thousands of investors into a common portfolio, an SIF creates individual portfolios for each investor but follows a systematic, rules-based investment approach.

SIFs are ideal for investors who want automated wealth creation but still prefer a tailored allocation strategy. These funds invest across equities, debt instruments, and hybrid assets depending on the investor’s profile and goals.

Here’s how SIF stands out:

Customization – Each investor’s portfolio is built based on their financial goals and risk appetite.

Systematic Approach – Regular, disciplined investing through periodic contributions, much like a SIP (Systematic Investment Plan).

Transparency & Control – Investors get real-time visibility of holdings and can modify their investment strategy when required.

Flexibility – No strict fund mandates like MFs; portfolio managers can adjust holdings dynamically.

In short, SIFs offer a blend of automation, personalization, and active management, making them an emerging choice among modern investors seeking higher efficiency than mutual funds but lower entry barriers than PMS or AIFs.

What is MF (Mutual Fund)?

A Mutual Fund (MF) is one of the most popular investment options in India, designed to make diversified investing accessible to everyone — from first-time investors to seasoned professionals. In a mutual fund, money from thousands of investors is pooled together and managed by a professional fund manager who invests it across stocks, bonds, or hybrid instruments, depending on the fund type.

What makes mutual funds appealing is their simplicity, affordability, and liquidity. You can start investing with as little as ₹500 through a Systematic Investment Plan (SIP), and easily redeem your units when needed.

Here’s what defines a Mutual Fund:

Low Entry Barrier – You can start small; perfect for retail investors.

Diversification – Risk is spread across many securities and sectors.

Professional Management – Managed by SEBI-registered fund managers.

Liquidity – Open-ended funds allow easy entry and exit at NAV-based prices.

Regulated & Transparent – Governed by SEBI with regular disclosures and fund fact sheets.

However, mutual funds offer limited customization — all investors in a fund share the same portfolio and returns. Compared to SIFs, which build tailored portfolios, MFs follow a common strategy for everyone.

In essence, mutual funds are best suited for individuals who prefer affordable, regulated, and low-maintenance investing, even if that means giving up personalization and active control.

What is PMS (Portfolio Management Services)?

Portfolio Management Services (PMS) is a customized investment solution designed for high-net-worth individuals (HNIs) who want personalized portfolio management and direct ownership of their investments. Unlike mutual funds, where all investors share a common pool, PMS creates a separate demat account for each investor, ensuring that the stocks and securities are owned individually.

Each PMS is managed by a professional portfolio manager who builds and actively manages your portfolio based on your risk profile, financial goals, and market outlook. The strategies can range from equity-focused to multi-asset approaches, giving investors greater flexibility and control.

Here’s what defines PMS:

Personalized Strategy – Portfolios are tailor-made based on the investor’s objectives, unlike MFs where one model fits all.

Direct Ownership – Securities are held in your name, ensuring full transparency.

Active Management – Portfolio managers can rebalance holdings quickly in response to market movements.

High Minimum Investment – Usually starts at ₹50 lakh (as per SEBI).

Performance-Linked Fees – Charges are based on returns, not just flat management fees.

Compared to SIFs, which offer systemized and flexible investing, PMS involves a hands-on, discretionary approach — ideal for investors who seek personal attention and higher return potential, and are comfortable with higher market exposure and costs.

In short, PMS sits between mutual funds and AIFs — combining professional expertise, active management, and individual control for serious investors.

Suggested Read: PMS vs Mutual Fund

What is AIF (Alternative Investment Fund)?

An Alternative Investment Fund (AIF) is a privately pooled investment vehicle that collects money from sophisticated and high-net-worth investors to invest in non-traditional assets such as private equity, venture capital, hedge funds, real estate, or debt instruments.

Unlike Mutual Funds or PMS, which primarily invest in listed securities, AIFs focus on alternative opportunities that are typically not accessible to retail investors. These funds aim for higher returns, but they also come with longer lock-in periods and higher risk due to the nature of the underlying assets.

Types of AIFs (as per SEBI classification):

Category I AIFs – Invest in startups, early-stage ventures, and infrastructure funds.

Category II AIFs – Include private equity funds, debt funds, and real estate funds.

Category III AIFs – Employ complex strategies such as hedge funds, derivatives, and leverage-based investments for higher returns.

Here’s what sets AIFs apart:

Exclusive Access – Invests in private market opportunities unavailable to the public.

High Entry Barrier – Minimum investment starts at ₹1 crore (as per SEBI).

High Return Potential – Targets superior returns compared to traditional investments.

Low Liquidity – Longer lock-in periods; suitable for investors with patience and capital stability.

Professional Management – Managed by fund managers with deep expertise in alternative assets.

In essence, AIFs are designed for ultra-high-net-worth investors who seek diversification beyond traditional equities and debt, and are ready to accept higher risk and illiquidity in pursuit of superior long-term returns.

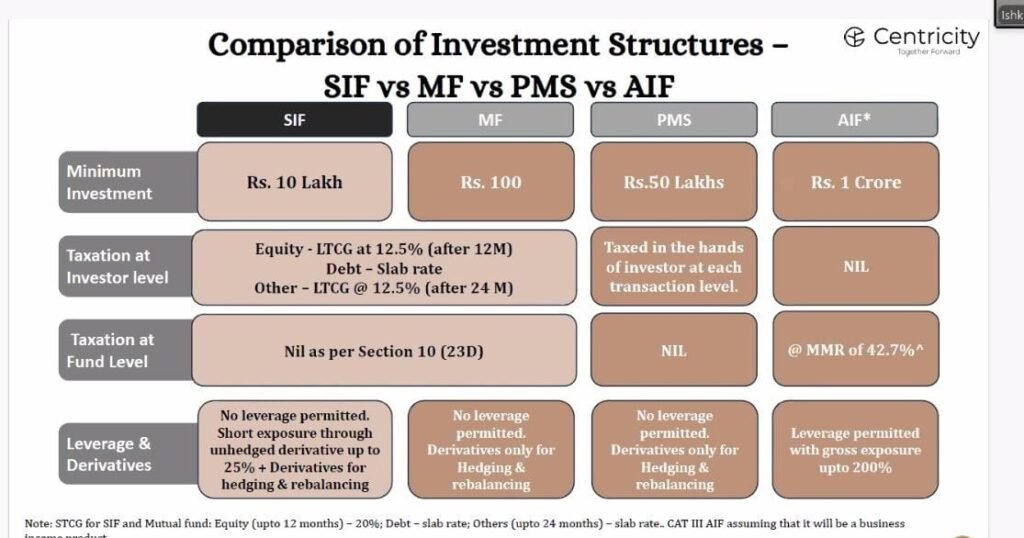

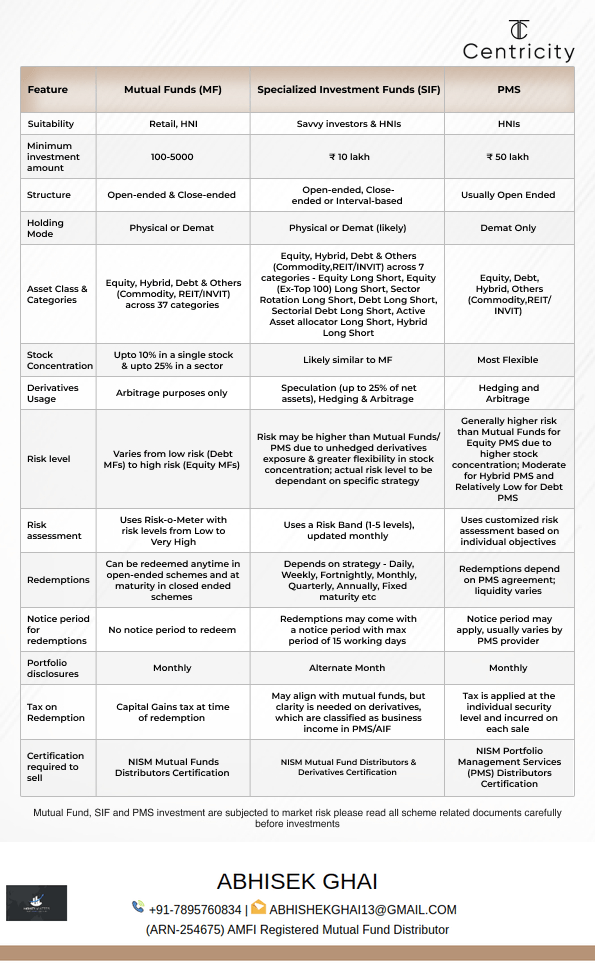

SIF vs MF vs PMS vs AIF — Key Differences at a Glance

| Feature / Parameter | SIF (Systematic Investment Fund) | MF (Mutual Fund) | PMS (Portfolio Management Service) | AIF (Alternative Investment Fund) |

|---|---|---|---|---|

| Minimum Investment | ₹10 lakh | ₹500 (SIP) – ₹1 lakh (lump sum) | ₹50 lakh | ₹1 crore |

| Investor Eligibility | Retail, mass affluent, HNI | Retail investors | High-net-worth individuals | Ultra HNIs / sophisticated investors |

| Ownership Structure | Individualized portfolio per investor | Pooled fund | Separate demat account per investor | Pooled fund (private investments) |

| Management Style | Systematic, semi-customized | Professionally managed, common portfolio | Fully discretionary, personalized | Professional, alternative strategies, private market focus |

| Risk Level | Moderate (depending on strategy) | Low–Moderate | Moderate–High | High |

| Liquidity | Moderate | High (open-ended) | Moderate (depends on strategy) | Low (long lock-ins) |

| Fees / Charges | Management + performance-linked (lower than PMS) | Fund management + expense ratio | Management + performance fee | High management + performance fee |

| Transparency | High | High (SEBI-regulated) | High (direct account) | Moderate–High (depends on reporting) |

| Taxation | Capital gains as per applicable slab | Capital gains per MF rules | Capital gains + short-term/long-term rules | Complex, depends on fund type & gains |

| Ideal For | Investors seeking systematic, semi-customized investing | Beginners & retail investors | HNIs seeking personalization | Ultra HNIs seeking alternative, high-return investments |

Which Investment Option is Right for You?

Choosing between SIF, MF, PMS, and AIF depends on your investment amount, risk appetite, financial goals, and level of involvement. Here’s a detailed guide for different investor profiles:

1. Retail Investors & Beginners

Recommended Options: Mutual Funds (MFs)

Why:

Low entry barrier (as low as ₹500 via SIP)

Diversified portfolios managed professionally

High liquidity and transparent reporting

Avoid: PMS and AIF due to high minimum investment and complexity

Optional: SIFs if you have ₹10 lakh and want semi-customized exposure

2. Mass-Affluent / Emerging High-Net-Worth Investors

Recommended Options: SIF or PMS

Why:

SIF offers systematic, semi-customized investing without huge capital

PMS gives personalized portfolio management for ₹50 lakh+ investors

Both allow higher control and better returns than standard mutual funds

Avoid: Category III AIFs unless you’re ready for high risk and illiquidity

3. High-Net-Worth & Ultra-HNW Investors

Recommended Options: PMS and AIF

Why:

PMS allows full discretionary management and direct ownership

AIFs unlock alternative investments like private equity, venture capital, and hedge strategies

Potential for higher returns, but also higher risk and longer lock-ins

Optional: SIFs for strategic diversification alongside AIF/PMS

4. Choosing Based on Goals & Risk Appetite

Capital Preservation / Moderate Growth: MFs or Category I/II AIFs

Aggressive Growth / Higher Returns: PMS or Category III AIFs

Systematic & Disciplined Approach with Flexibility: SIF

Pros & Cons of SIF, MF, PMS, and AIF

1. Mutual Funds (MFs)

Pros:

Low minimum investment; accessible to all

Professionally managed and SEBI-regulated

High liquidity; easy redemption

Diversified portfolio reduces risk

Simple and convenient for beginners

Cons:

Limited customization; same portfolio for all investors

Returns may be moderate compared to PMS or AIF

Less control over individual holdings

2. Systematic Investment Funds (SIFs)

Pros:

Semi-customized portfolios based on investor profile

Systematic approach reduces market timing risk

Transparent and monitored professionally

Bridges gap between mutual funds and PMS

Cons:

Higher minimum investment (₹10 lakh) than MFs

Moderate liquidity compared to MFs

Slightly higher fees than standard mutual funds

3. Portfolio Management Services (PMS)

Pros:

Fully customized portfolio based on individual goals

Active management allows quick rebalancing and optimization

Direct ownership of securities; high transparency

Higher return potential than MFs

Cons:

High minimum investment (₹50 lakh+)

Management and performance-linked fees can be expensive

Requires some level of financial sophistication

4. Alternative Investment Funds (AIFs)

Pros:

Access to private equity, real estate, hedge funds, and venture capital

Potential for superior long-term returns

Professionally managed by expert fund managers

Diversifies risk beyond traditional asset classes

Cons:

Very high minimum investment (₹1 crore+)

Longer lock-in periods; low liquidity

Higher risk; not suitable for average retail investors

Complex taxation and reporting

Latest Developments & 2025 Trends in SIF, MF, PMS, and AIF

The Indian investment landscape is evolving rapidly, and staying updated is crucial for making informed decisions. Here’s what investors need to know in 2025:

1. SIF (Systematic Investment Fund) Trends

Rising Popularity: More mass-affluent and HNI investors are adopting SIFs due to their hybrid approach between MFs and PMS.

Flexible Entry Points: Several fund houses now allow lower minimum investments to attract emerging HNIs.

Technology Integration: Digital platforms are enabling automated portfolio tracking, rebalancing, and reporting for SIF investors.

2. Mutual Funds (MFs) Trends

SIP Growth Continues: Systematic Investment Plans are becoming the preferred route for retail investors, with monthly contributions exceeding ₹10,000 crore collectively.

Hybrid & Thematic Funds: Investors increasingly prefer sectoral, ESG, and thematic funds, beyond standard equity and debt options.

Regulatory Updates: SEBI mandates more transparent risk disclosure and fund performance reporting, improving investor confidence.

3. Portfolio Management Services (PMS) Trends

Customized Solutions in Demand: PMS offerings are increasingly personalized based on investor goals and risk appetite.

Integration of AI & Analytics: Advanced portfolio analytics, predictive modeling, and algorithmic suggestions are becoming common in PMS.

Expanding HNI Access: Platforms are lowering minimum ticket sizes slightly, attracting emerging high-net-worth individuals.

4. Alternative Investment Funds (AIFs) Trends

Category I & II AIFs Growing: Early-stage venture capital, private equity, and real estate funds are attracting more investors due to potentially higher returns.

Category III AIFs Innovation: Hedge funds and algorithmic investment strategies are expanding, especially for sophisticated investors.

Regulatory Oversight: SEBI continues to refine compliance norms, making AIFs more transparent and structured.

Key Takeaways for 2025

SIFs are emerging as the bridge for mass-affluent investors, offering systematic investing with some personalization.

Mutual Funds remain the best choice for retail investors due to liquidity and low entry barriers.

PMS offers highly personalized strategies for HNIs seeking active management.

AIFs continue to dominate for ultra-HNIs targeting alternative assets with high return potential.