What is AIF? Meaning, Categories, Regulations & Benefits (2025 Guide)

Alternative Investment Funds (AIFs) have become one of the most preferred investment options for HNIs, UHNIs, and family offices in India—mainly because they offer access to specialized, high-growth, and alternative asset classes that traditional products like mutual funds cannot provide. As India’s wealth management space evolves, AIFs are gaining stronger traction, with SEBI reporting continuous year-on-year growth in commitments and total AUM across all three categories.

So, what is AIF?

An AIF is a privately pooled investment vehicle regulated by SEBI that collects funds from sophisticated investors and invests them according to a defined strategy. These strategies can include private equity, venture capital, real estate, pre-IPO investments, long–short equity, credit opportunities, distressed assets, and more.

In this 2025 guide, we break down the meaning of AIF, how it works, updated SEBI regulations, types of AIFs, taxation rules, AIF vs PMS differences, and the list of top AIFs in India to help you understand whether this investment class is right for you.

What is AIF? (AIF Meaning Explained in Simple Terms)

An Alternative Investment Fund (AIF) is a privately pooled investment vehicle that collects money from investors and invests it in alternative asset classes outside traditional markets like stocks, bonds, and mutual funds. AIFs are regulated by SEBI under the AIF Regulations, 2012, with continuous amendments up to 2025, ensuring transparency, investor protection, and accountability.

In simple terms, AIFs allow investors—especially HNIs and institutions—to participate in high-growth, specialized investment opportunities such as:

Private Equity & Venture Capital

Real Estate Projects

Hedge Fund–style Long–Short Strategies

Private Credit & Structured Debt

Distressed or Special Situation Assets

Pre-IPO investments

Infrastructure & SME investments

These are opportunities not available in regular retail investment products.

Why AIFs Exist

Traditional financial products often limit upside potential or restrict access to emerging opportunities. AIFs were introduced to:

Support early-stage businesses and India’s startup ecosystem

Channel sophisticated capital toward sectors like real estate, credit, and infrastructure

Provide investors with access to high-growth and non-correlated assets

Expand diversification beyond public markets

Who Can Invest in an AIF?

AIFs are meant for sophisticated, high-net-worth investors, with SEBI requiring:

Minimum investment: ₹1 crore (₹25 lakh for employees/directors of the AIF)

Only resident Indians, NRIs, and foreign investors meeting eligibility norms can participate

Because of their complexity and risk, AIFs are not suitable for average retail investors.

How AIFs Are Structured

AIFs typically operate in the form of a trust, managed by:

Sponsor (promoter of the fund)

Trustee (ensures compliance)

Investment Manager (makes investment decisions)

This structure makes AIFs professionally managed, highly regulated, and strategically disciplined.

How Do AIFs Work?

Alternative Investment Funds operate through a structured, regulated, and professionally managed investment process designed for sophisticated investors. Unlike mutual funds, AIFs follow a commitment-based model, invest in less liquid but high-potential opportunities, and deploy capital over time based on the fund’s strategy.

Below is a simple explanation of how AIFs function from start to finish.

1. Capital is Raised from Eligible Investors

AIFs raise money from:

High-Net-Worth Individuals (HNIs)

Ultra-HNWIs

Family offices

Institutional investors

Eligible foreign investors

Each investor must commit at least ₹1 crore (as per SEBI guidelines). This ensures only informed investors enter the scheme.

2. The AIF Manager Deploys Capital According to a Defined Strategy

Every AIF is launched with a clearly stated investment thesis, such as:

Venture capital or early-stage startups

Private equity in growing companies

Real estate or infrastructure projects

Private credit and structured debt

Hedge fund–style long–short market strategies

Distressed or special situations investing

The investment manager makes decisions, conducts due diligence, and executes the strategy on behalf of investors.

3. Funds Operate Through a Commitment & Drawdown System

Instead of paying the full amount upfront, investors make a capital commitment.

The AIF then draws down money in phases as investment opportunities arise.

This structure allows:

Better capital efficiency

Controlled deployment

Timely entry into opportunities

4. Professional Management & Governance

An AIF is governed through:

Sponsor – sets up and backs the fund

Trustee – ensures compliance and investor protection

Investment Manager – runs the strategy

Custodian (mandatory for Category III) – holds assets

Auditors – ensure financial transparency

This creates a multi-layered governance model ensuring strict oversight.

5. Returns Are Distributed After Exit

AIF returns are realized when the fund exits its investments via:

Business sale

IPO

Secondary sale

Asset sale

Debt repayment

Market-based exits (Category III)

Distributions follow a waterfall structure, usually:

Return of capital

Preferred return (if applicable)

Profit share (carry) for the fund manager

6. Lock-In and Liquidity

AIFs are illiquid investments, especially Category I & II.

Investors remain locked-in until the fund tenure ends (typically 5–10 years).

Category III AIFs may offer higher liquidity, depending on strategy.

7. Reporting & Transparency

Per SEBI regulations (updated to 2025):

AIFs must provide quarterly reports

Disclose risk, leverage (Category III), and portfolio exposures

Maintain valuation as per SEBI-prescribed standards

This keeps investors consistently informed.

Types of AIFs in India (Category I, II & III Explained)

SEBI classifies Alternative Investment Funds into three categories, each designed for different types of investment strategies, risk levels, and economic impact. Understanding these categories is crucial because the returns, risk exposure, investment horizon, and even taxation rules vary significantly across them.

Below is a simple and updated explanation of all three AIF categories as per SEBI regulations (amended till 2025).

Category I AIFs

Category I AIFs invest in sectors that promote India’s economic growth and innovation. These funds support early-stage companies, infrastructure, social ventures, and government-approved sectors.

What Category I AIFs Invest In

Venture Capital (VC)

Angel Funds

SME Funds

Social Venture Funds

Infrastructure Funds

Startup-focused investment schemes

Risk Level: Moderate to High

Investor Profile: Investors seeking long-term, high-growth investments

Tenure: Commonly 7–10 years

Leverage: Not permitted

Taxation: Pass-through for most income components

Category I = Growth + Economic Impact + Long-Term Returns

Category II AIFs

Category II is the largest and most diverse segment in India’s AIF ecosystem. It includes funds that do not fall under Category I or III but invest in long-term opportunities without leveraging or employing complex trading strategies.

What Category II AIFs Invest In

Private Equity (PE)

Debt/Private Credit Funds

Real Estate Funds

Distressed Asset/Special Situation Funds

Structured Credit

Mezzanine Financing

Risk Level: Moderate (Credit/Real Estate) to High (PE/Distressed)

Investor Profile: Investors seeking stable long-term alternative assets

Tenure: Typically 6–9 years

Leverage: Not allowed

Taxation: Pass-through (except business income)

Category II = Long-Term + Stable Alternatives + High Governance

Category III AIFs

Category III funds use advanced strategies to generate returns in both rising and falling markets. These are the most flexible AIFs and often similar to hedge funds.

What Category III AIFs Invest In

Long–Short Equity Strategies

Arbitrage

Derivatives & Structured Products

Quant/Algo Strategies

Market-Neutral & Hedged Portfolios

High-frequency or tactical trades

Risk Level: Moderate to Very High (depending on leverage & strategy)

Leverage: Permitted within SEBI-defined limits

Investor Profile: Investors comfortable with market-linked volatility and dynamic strategies

Tenure: Usually open-ended or 3–5 years

Taxation: No pass-through; income taxed at investor level as business income or capital gains

Category III = Hedge-Fund Style + Tactical + High Agility

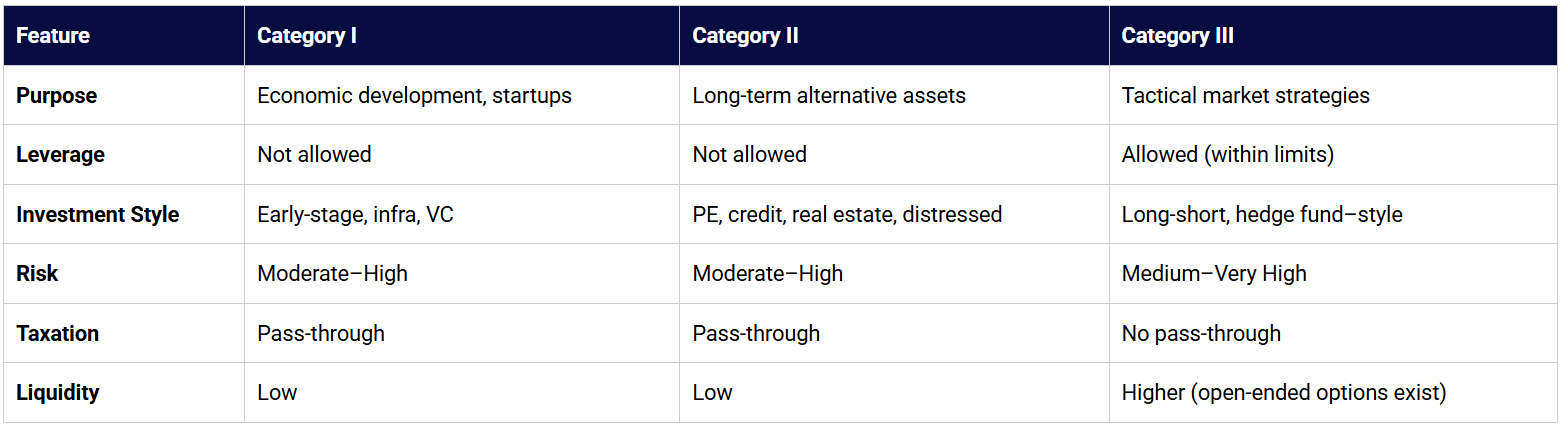

Key Differences Between Category I, II & III AIFs

| Feature | Category I | Category II | Category III |

|---|---|---|---|

| Purpose | Economic development, startups | Long-term alternative assets | Tactical market strategies |

| Leverage | Not allowed | Not allowed | Allowed (within limits) |

| Investment Style | Early-stage, infra, VC | PE, credit, real estate, distressed | Long-short, hedge fund–style |

| Risk | Moderate–High | Moderate–High | Medium–Very High |

| Taxation | Pass-through | Pass-through | No pass-through |

| Liquidity | Low | Low | Higher (open-ended options exist) |

Best Performing Multi Cap PMS in India (2025)

Multi Cap PMS portfolios invest across large, mid, and small-cap companies, offering a balance of stability, growth momentum, and high-return potential. These portfolios typically aim to generate alpha (returns above benchmark indices) by identifying early-stage leaders in emerging sectors.

Below is a performance comparison of the top-performing Multi Cap PMS strategies, based on their 1Y, 3Y, 5Y returns, AUM, and portfolio allocation across market caps.

AIF Regulations in India (SEBI 2025 Updated Rules)

Alternative Investment Funds in India operate under a strict regulatory framework governed by the SEBI (Alternative Investment Funds) Regulations, 2012, with multiple amendments up to September 2025. These regulations ensure transparency, investor protection, risk management, and proper governance—making AIFs one of the most tightly monitored investment structures in the country.

Below are the key SEBI regulations every investor should know in 2025.

1. Mandatory Registration of AIFs

Every AIF must be registered with SEBI under one of the three categories:

Category I

Category II

Category III

Registration ensures oversight, reporting, and compliance with the fund’s stated strategy.

2. Minimum Investment Requirement

To ensure only sophisticated investors participate:

Minimum investment remains ₹1 crore per investor

Employees and directors of the fund can invest as low as ₹25 lakh

Accredited investors may qualify under relaxed norms depending on SEBI-approved frameworks

This rule ensures retail investors are protected from high-risk alternative investments.

3. Sponsor Commitment (Skin-in-the-Game Norms)

SEBI mandates sponsors/managers to invest in their own fund:

Minimum 2.5% of the fund corpus or

₹5 crore, whichever is lower

This aligns the interests of fund managers with investors.

In 2025 amendments, SEBI strengthened disclosures around sponsor commitment dilution and transfer.

4. Restrictions on Leverage

Category I & II AIFs: No leverage permitted, except for temporary borrowings (up to 30 days, not exceeding four times a year).

Category III AIFs: Leverage allowed as per SEBI-prescribed risk and leverage limits; must maintain a comprehensive risk management framework.

This ensures systemic risk is controlled across the industry.

5. Valuation & NAV Disclosure Rules

SEBI mandates:

Quarterly or monthly NAV disclosure (depending on fund structure)

Independent valuation by SEBI-registered valuation agencies

Category III AIFs must follow tighter risk and valuation reporting due to their dynamic strategies

Higher transparency reduces information risk for investors.

6. Reporting Requirements

AIFs must submit:

Quarterly reports to SEBI

Annual audit reports

Portfolio disclosures to investors

Leverage and risk reports (Category III)

Regulatory filings via SEBI’s centralised reporting portal

These updates help SEBI monitor market exposure and ensure early detection of risk.

7. Restrictions on Fund Tenure & Extensions

Category I & II AIFs: Closed-ended only

Category III AIFs: Can be open-ended or closed-ended

Extension norms require:

Investor consent (min. 2/3rd by value) OR

SEBI approval in exceptional cases

This prevents indefinite locking of investor capital.

8. Investment Concentration Limits

Exposure caps ensure diversification and prevent concentration risk

Category I & II must adhere to limits on investing in a single company or group

Category III funds follow position and exposure limits similar to PMS/hedge-fund frameworks

9. Regulations on Related-Party Transactions

AIFs must follow strict regimes:

No investment in associates without approval

Mandatory disclosure of conflicts of interest

Independent oversight by trustee/custodian

This enhances fiduciary protection.

10. Investor Protection Measures (2025 Updates)

Recent SEBI circulars introduced:

Stricter valuation rules for private credit and special situation funds

Classification norms for hybrid and complex funds

Enhanced risk summaries and easier-to-read investor documents

Stronger guardrails for Category III funds using derivatives

These ensure transparency in risk-heavy alternative strategies.

In Summary:

SEBI’s 2025 regulations aim to:

Improve transparency

Strengthen governance

Reduce leverage risks

Enhance investor protection

Standardize valuation practices

Ensure responsible fund management

Market Allocation Trends in PMS Portfolios (2025)

One of the biggest factors influencing PMS performance is how the portfolio is allocated across Large Cap, Mid Cap, and Small Cap stocks. Each market segment behaves differently based on market cycles, liquidity, and earnings growth visibility:

Large Caps → Stability, lower volatility, steady compounding

Mid Caps → Growth potential with moderate volatility

Small Caps → Higher return potential but higher short-term fluctuations

The allocation data from the analyzed PMS portfolios reveals distinct investment styles across Large Cap and Multi Cap PMS strategies.

AIF Structure: How an AIF Fund is Set Up

The structure of an Alternative Investment Fund (AIF) is designed to offer strong governance, transparency, and regulatory compliance. SEBI mandates a defined hierarchy of entities and responsibilities, ensuring that investor capital is professionally managed and protected at every stage. Below is a simplified explanation of how an AIF is typically set up in India.

The Sponsor is the founding entity responsible for creating the AIF. They contribute the required minimum “skin-in-the-game” capital and ensure that the fund meets SEBI’s eligibility criteria. Sponsors are usually experienced financial institutions, wealth management firms, or established investment professionals who have the credibility to launch and back the fund.

The Trustee plays a crucial oversight role, especially when the AIF is created in a trust structure, which is the most common format in India. The trustee ensures that the fund operates strictly within SEBI’s regulations and acts in the best interest of investors. They review and approve key decisions taken by the investment manager, maintain compliance oversight, and act as an independent guardian of investor rights.

The Investment Manager is the core operator of the AIF. This entity or team defines the investment strategy, conducts due diligence, selects deals, manages risk, and executes exits. They are responsible for day-to-day decisions and for meeting the return expectations laid out in the fund’s mandate. SEBI’s 2025 framework places significant responsibility on investment managers for accurate valuation, risk management, and transparent reporting.

The Fund Entity itself can be set up as a trust, company, or LLP, depending on the strategy and operational preference. However, trust structures remain the most popular due to their flexibility and tax efficiency. The fund entity holds investor commitments and houses the investment portfolio.

For Category III AIFs, appointing a Custodian is mandatory. Custodians manage the safekeeping of securities, execute settlements, maintain asset segregation, and support regulatory reporting—an essential requirement given the leveraged or trading-heavy nature of Category III strategies. Many Category II AIFs also voluntarily appoint custodians for enhanced transparency and operational efficiency.

Auditors and Registered Valuers are additional independent parties involved in the fund’s governance. The auditor reviews annual financial statements, ensuring compliance and accuracy, while the valuer provides unbiased valuations of portfolio companies or assets. SEBI has strengthened valuation norms through 2025 amendments to standardize valuation practices across the industry.

Finally, Investors, known as Limited Partners (LPs), provide the capital commitments. These investors typically include HNIs, UHNIs, family offices, corporates, institutions, and eligible foreign investors. Their capital is deployed by the AIF over time, and they receive regular reports, updates, and eventual profit distributions based on the fund’s performance and exit strategy.

In terms of lifecycle, an AIF moves through phases including fundraising, capital deployment, portfolio monitoring, exits, distributions, and final closure. Depending on the category and strategy, the tenure of an AIF generally ranges from three to ten years, with Category I and II being closed-ended and Category III offering both closed and open-ended structures.

Overall, an AIF is built on a robust, multi-layered structure involving the sponsor, trustee, investment manager, custodian, auditor, valuer, and investors—all functioning together to ensure efficient fund management, regulatory compliance, and investor protection.

Who Should Invest in an AIF? (Ideal Investor Profile)

Alternative Investment Funds are designed primarily for sophisticated, high-net-worth investors who understand complex investment strategies and are comfortable with longer lock-in periods. SEBI has intentionally restricted AIF access to investors with a minimum commitment requirement of ₹1 crore, ensuring that only individuals or institutions with sufficient financial capacity and risk tolerance participate. Because AIFs invest in private equity, venture capital, private credit, real estate, and high-level market strategies, they suit investors who want exposure beyond traditional equity and debt portfolios.

AIFs are ideal for HNIs and UHNIs who seek diversification into high-growth or uncorrelated asset classes that are not available through mutual funds or retail investment products. These investors typically possess the financial cushion to absorb medium-to-high levels of risk and can commit capital for longer durations, often ranging between five to ten years, depending on the fund category.

They are also well-suited for family offices, which often allocate capital strategically across private markets, alternative assets, and long-term value-creation opportunities. AIFs help such entities broaden their portfolio exposure and access professionally managed, high-potential deals in sectors like private equity, real estate, and venture capital.

Additionally, institutional investors—such as corporates, NBFCs, banks (subject to regulatory limits), and trusts—frequently participate in AIFs to enhance returns and achieve portfolio diversification. These entities value the structured risk management, governance frameworks, and transparency that AIFs offer under SEBI’s regulatory oversight.

AIFs are recommended for investors with a higher risk appetite, as these funds may involve illiquidity, market volatility, delayed exits, leverage (in Category III), or concentrated bets depending on the strategy. Investors must be comfortable with the idea that returns are often realized only at the end of the fund tenure, and interim liquidity may be limited.

However, AIFs are not suitable for beginners or conservative investors who prefer steady income, low volatility, or easy redemption. The complexity, risk level, and high entry threshold make AIFs appropriate only for investors who understand private markets, alternative strategies, and long-term commitment cycles.

In summary, AIFs are an excellent choice for experienced investors who want to expand beyond traditional markets, seize specialized opportunities, and build a diversified portfolio backed by professional fund management.

Benefits of AIFs (Why HNIs Prefer AIFs)

AIFs offer investors access to high-potential, alternative asset classes that go beyond traditional markets. Here are the key benefits explained in short, clear pointers:

• Access to Exclusive Opportunities:

Invest in private equity, venture capital, pre-IPO deals, private credit, real estate, and hedge-fund-style strategies unavailable to retail investors.

• Higher Diversification:

AIFs reduce portfolio concentration by adding non-correlated assets that behave differently from stock and bond markets.

• Professionally Managed Strategies:

Experienced investment managers use in-depth research, deal networks, and advanced strategies to identify high-quality opportunities.

• Potential for Superior Long-Term Returns:

Private markets and alternative assets often generate alpha that may outperform public market benchmarks over longer periods.

• Flexibility in Investment Strategies:

Category I, II, and III AIFs offer a wide spectrum—from early-stage investing to credit, real estate, distressed assets, and long–short equity.

• Lower Short-Term Volatility:

Many Category II AIFs (like private equity or credit funds) are less affected by short-term market swings due to their private-market nature.

• Regulated and Transparent Structure:

AIFs are tightly regulated by SEBI with strict disclosure, valuation, and reporting standards, ensuring high transparency.

• Portfolio Customization for Institutions & Family Offices:

AIFs allow sophisticated investors to fine-tune asset allocation based on risk appetite, sector preferences, and long-term goals.

• Strong Governance Framework:

Auditors, custodians, trustees, and independent valuers ensure compliance, transparency, and protection of investor interests.

Risks & Limitations of AIFs (What Investors Must Know)

While AIFs offer high-growth opportunities, they also come with meaningful risks that investors must understand before committing capital. Here are the key limitations explained in short, clear pointers:

• High Minimum Investment Requirement:

AIFs require a minimum investment of ₹1 crore, making them suitable only for HNIs, UHNIs, and institutional investors.

• Limited Liquidity:

Category I and II AIFs are closed-ended with long lock-in periods. Investors cannot exit anytime and must wait until the fund reaches maturity or completes its exit cycle.

• Long Investment Horizon:

Most AIFs have tenures of 5–10 years, meaning capital remains committed for an extended duration without frequent liquidity events.

• Higher Risk Exposure:

Private equity, venture capital, special situation funds, and long–short strategies involve higher risk compared to traditional investment products.

• Market Volatility (Category III AIFs):

Category III AIFs, which deploy complex long–short or derivative strategies, may experience higher volatility due to market movements and leverage.

• Illiquid Underlying Assets:

Many AIFs invest in private companies, real estate, credit deals, or distressed assets—markets that do not offer quick or easy exits.

• Dependence on Fund Manager Expertise:

Returns largely depend on the skill, strategy, and judgment of the investment manager. A weak manager or poorly executed strategy can significantly impact performance.

• Higher Fees:

AIFs often follow a 2–20 fee structure (management fee + performance fee), which may reduce net returns if performance is inconsistent.

• Regulatory & Compliance Risks:

Changes in SEBI regulations, taxation rules, or RBI limits on institutional investments can impact fund operations and investor returns.

• Uncertain Exit Timelines:

Private market exits depend on valuations, buyer interest, economic conditions, and liquidity events such as IPOs or acquisitions, which may take longer than expected.

AIF vs PMS: Key Differences (2025 Overview)

AIFs and PMS are both popular investment options for HNIs, but they function very differently. PMS focuses on personalized equity and debt portfolios, while AIFs give access to specialized alternative investments like private equity, venture capital, private credit, real estate, and long–short strategies.

• Investment Structure:

PMS creates a separate, customized portfolio for each investor, whereas AIFs pool money from multiple investors into a single fund.

• Minimum Investment:

Both require ₹50 lakh for PMS and ₹1 crore for AIFs, as per SEBI regulations.

• Strategy & Asset Classes:

PMS mostly invests in listed equities or debt. AIFs invest in private markets, hedge strategies, structured credit, startups, and high-growth assets.

• Liquidity:

PMS offers better liquidity since investors hold stocks directly. AIFs, especially Category I & II, have long lock-ins and limited exit windows.

• Risk & Return Profile:

PMS returns depend on market performance, while AIF returns rely heavily on the fund manager’s skill and the performance of private or alternative assets.

• Taxation:

PMS taxation is similar to direct equity. AIF taxation varies by category—Category I & II offer pass-through benefits, while Category III is taxed at the investor level.

In short:

PMS is suitable for investors wanting personalized equity portfolios, while AIFs are designed for those seeking diversified, high-potential alternative investments.

Suggested Content:

SIF vs MF vs PMS vs AIF

PMS Vs Mutual Fund

PMS/AIF

Taxation of AIFs in India (2025 Updated Rules)

Taxation of Alternative Investment Funds in India varies significantly depending on the category of the AIF. SEBI and the Income Tax Act apply different rules for Category I, II, and III funds, so it’s important for investors to understand how returns will be taxed before they commit capital.

For Category I and Category II AIFs, taxation follows a pass-through structure. This means the income generated by the fund is taxed directly in the hands of the investors and not at the fund level (except business income). Capital gains—short-term or long-term—retain their nature and are taxed as per applicable rates for the investor. Business income earned by the fund, however, is taxed at the fund level itself.

For Category III AIFs, the pass-through benefit is not available. Category III funds are taxed similar to a business entity because they frequently trade in equities, derivatives, and complex strategies. Any gains from listed securities or market-linked instruments may be treated as business income, depending on the fund’s structure. This income is then taxed at the applicable rate for the fund, and the net amount is distributed to investors. Long-term and short-term capital gains may still apply in certain structures, but the treatment largely depends on whether the AIF operates as a trust or a company.

Resident and non-resident investors may also be subject to TDS (Tax Deducted at Source) depending on the nature of income. Additionally, foreign investors in AIFs may benefit from DTAA (Double Taxation Avoidance Agreements) depending on their country of residence.

In summary, Category I & II AIFs offer more tax efficiency due to pass-through benefits, while Category III AIFs have more complex taxation due to trading activity and business income classification. Investors should always evaluate taxation impact along with the fund’s strategy and risk level.

Top AIFs in India (2025 List)

India’s AIF industry continues to expand rapidly, with strong participation from domestic fund houses, global asset managers, wealth platforms, and specialized private market firms. While SEBI does not publish “rankings,” several AIFs are widely recognized in the industry for their scale, strategy expertise, and established track record.

Below is a 2025-ready list of well-known AIFs in India, grouped by category, to help investors understand the leading players in the ecosystem.

Category I AIFs (Venture Capital & Startup-Focused)

Category I funds are known for investing in early-stage startups, SMEs, infrastructure, and sectors that support economic growth.

• Chiratae Ventures India Fund

• Nexus Venture Partners AIF

• Blume Ventures AIF

• India Quotient AIF

• 3one4 Capital AIF

• Kalaari Capital AIF

• Sixth Sense Ventures AIF

• Elevation Capital (Previously SAIF Partners) AIF

These funds are generally associated with technology, consumer brands, and emerging sectors.

Category II AIFs (Private Equity, Credit, Real Estate & Special Situations)

Category II is the broadest category and includes some of India’s largest AIFs by commitments and AUM.

• Kotak Special Situations Fund

• Motilal Oswal PE AIF

• ICICI Venture AIF

• Edelweiss Special Opportunities Fund

• IIFL Special Opportunities Series

• True North PE AIF

• Blackstone India-focused AIF structures

• JM Financial Credit Solutions AIF

• ASK Real Estate AIF

• Axis RERA Real Estate Fund

These funds invest in private equity, credit, real estate, infrastructure, and distressed assets.

Category III AIFs (Long–Short, Hedge Fund Strategies & Quant Funds)

Category III funds are known for dynamic, market-driven strategies targeting both rising and falling markets.

• Avendus Absolute Return Fund

• IIFL Multi-Strategy AIF

• Edelweiss Long-Short Fund

• Tata Long-Short Equity AIF

• ASK Golden Decade Long-Short AIF

• ICICI Prudential Long Short Fund

• Helios India Rising AIF

• Anandrathi Long-Short Strategy

These funds typically operate with higher liquidity compared to Category I & II.

Important Note for Users

This list represents well-known AIFs based on industry presence and category relevance, not rankings or performance indicators.

SEBI mandates strict disclosures for AIFs, but performance data and private-market valuations are not publicly distributed, so investors must always review:

Latest PPM (Private Placement Memorandum)

Track record documents

Risk disclosures

Fee structure

SEBI filings before investing.

Top 10 AIFs in India (2025)

Avendus Absolute Return Fund (Category III)

Kotak Special Situations Fund (Category II)

IIFL Special Opportunities Fund (Category II)

Motilal Oswal Private Equity AIF (Category II)

Chiratae Ventures India Fund (Category I)

Blume Ventures AIF (Category I)

Edelweiss Alternative Equity Scheme – Long/Short Fund (Category III)

Helios India Rising Fund (Category III)

ASK Real Estate AIF (Category II)

True North AIF (Category II)

Alternative Investment Funds (AIFs) have emerged as one of the most powerful investment avenues for HNIs, UHNIs, family offices, and institutions seeking exposure beyond traditional markets. With access to private equity, venture capital, private credit, real estate, and hedge-fund-style strategies, AIFs provide diversification, long-term growth potential, and professionally managed opportunities that are not available through regular investment products.

At the same time, AIFs come with higher risk, long lock-in periods, and a substantial minimum investment requirement of ₹1 crore. This makes them suitable primarily for experienced investors who understand private markets and are comfortable committing capital for several years. SEBI’s regulatory framework—updated till 2025—ensures transparency, governance, and investor protection, making AIFs a well-structured and credible investment category in India’s alternative ecosystem.

For investors looking to expand their portfolios, enhance diversification, and tap into high-potential opportunities, AIFs can be a compelling option when chosen carefully and aligned with personal financial goals and risk appetite.

Need Expert Guidance