Digital Gold vs Gold ETF: Which One Should You Choose in 2025?

Investing in gold has always been seen as a safe and reliable way to preserve wealth — but in 2025, you no longer need to buy physical gold bars or coins to do it. Two popular modern options — Digital Gold and Gold ETFs (Exchange Traded Funds) — have made gold investment easier, safer, and more transparent for everyone. Yet, for many investors, the real question remains: Digital Gold vs Gold ETF — which one is better?

In this guide, we’ll break down everything you need to know before investing — from how Gold ETFs work to what Digital Gold actually means, along with key differences in returns, liquidity, taxation, safety, and long-term potential. You’ll learn how both options function, how they fit into different financial goals, and which one aligns best with your investment style.

By the end, you’ll have a clear answer to the ongoing debate — Gold ETF vs Digital Gold — and understand which form of gold investment gives you better value and security. Plus, we’ll show how Money Matter can help you make the right choice based on your financial needs and market trends.

What Is Digital Gold and How Does It Work?

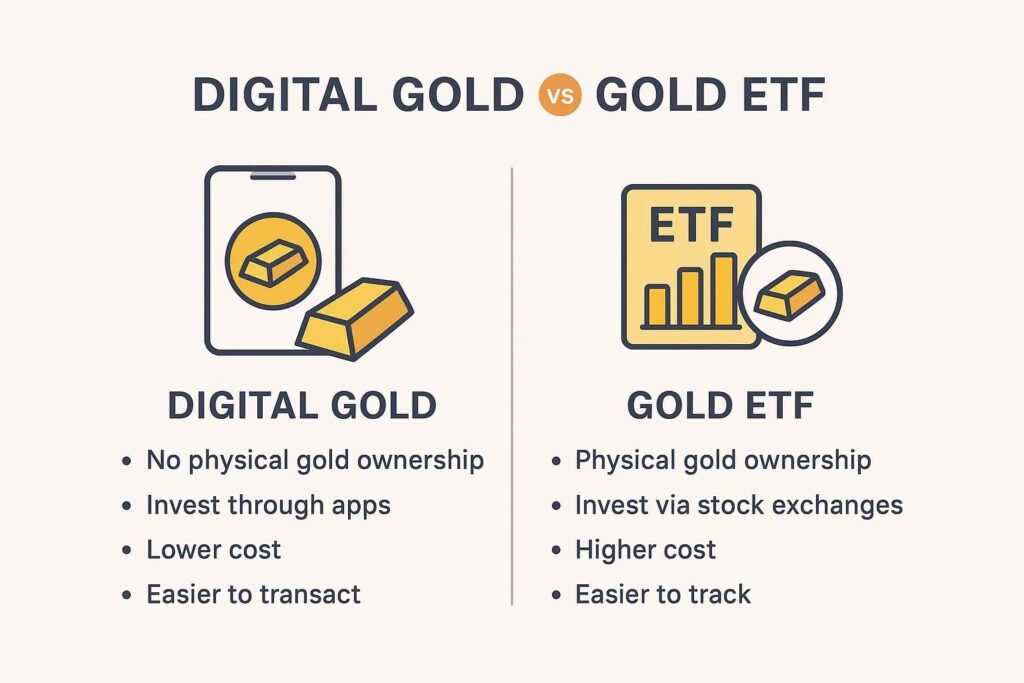

Digital Gold is a modern way to own gold without physically holding coins, bars, or jewelry. With just a few clicks on your phone, you can buy fractions of 24-carat (999 purity) gold which is stored securely in insured vaults by trusted custodians. Platforms like MMTC-PAMP, SafeGold, and Augmont manage this vaulting and storage; when you buy digital gold, the equivalent physical gold is allocated to you.

Key Features & Mechanics

Minimum Investment & Fractional Ownership: You can start very small—some platforms let you invest with as little as ₹10 or ₹100. This lowers the barrier to entry compared to physical gold.

Real-Time Pricing & Charges: Prices track live gold spot rates, but include additional costs—GST (often 3%), platform mark-ups, vaulting and insurance fees. These charges vary by platform and affect your effective buying price.

Storage & Custody: Your digital gold is held in vaults operated by custodians who maintain physical 24-carat gold, audited and insured. While you “own” that gold digitally (you have allotted physical gold in vaults), physical delivery is possible, often subject to minimum weight criteria, delivery fees, and waiting periods.

Liquidity & Redemption: You can sell digital gold on the platform at live rates. Some platforms allow converting digital gold to physical form (coins, bars or jewelry), though there are delivery charges and minimum threshold weights.

Market Trends & Adoption in India (2024-2025)

Digital gold via UPI channels has seen a 377% rise in transaction volume between April 2024 and August 2025, growing from around 20.9 million transactions to ~99.77 million transactions in August 2025.

The value of those purchases more than doubled — from approx ₹550 crore to ₹1,184 crore in the same period.

The price per gram of 24K gold has also risen by ~44% YoY, reaching around ₹11,021 per gram in August 2025 (for 24-carat) compared to ~₹7,633 a year earlier.

Pros & Important Limitations

Digital Gold offers ease, flexibility, very low minimums, and avoids many problems of physical gold (storage, purity, theft). But there are caveats: some platforms may have higher markups, regulatory oversight is less strong compared to SEBI-regulated Gold ETFs, and physical delivery has costs and minimum limits.

What Is a Gold ETF and How Does It Work?

A Gold ETF (Exchange Traded Fund) is a financial instrument that tracks the real-time market price of physical gold and allows investors to gain exposure to gold without having to store it physically. Each unit of a Gold ETF represents roughly 1 gram of 24-carat gold, and these units are traded on stock exchanges just like company shares.

How Gold ETFs Function

When you invest in a Gold ETF, your money is pooled with other investors’ funds and used by the Asset Management Company (AMC) to buy physical gold of 99.5% purity, stored securely in vaults under the custody of a regulated trustee. This ensures transparency and safety — every unit you hold is backed by actual gold stored in an RBI-approved vault.

Gold ETFs are listed and traded on the NSE and BSE, and you can buy or sell them anytime during market hours using your Demat and trading account. Prices fluctuate in line with live gold rates, meaning your investment mirrors the real-time movement of gold prices globally.

Why Gold ETFs Are Growing in Popularity (2025 Insights)

In 2025, India’s Gold ETF AUM (Assets Under Management) has surpassed ₹30,000 crore, marking an impressive 18% growth compared to 2024, as more investors shift toward regulated and liquid gold investment options. This surge has been fueled by rising inflation, global market uncertainty, and investors preferring paper gold over physical assets.

Additionally, Gold ETFs have become a popular hedge in diversified portfolios. Many financial planners recommend allocating 5–10% of investment portfolios to gold ETFs as a protection against currency depreciation and stock market volatility.

Key Advantages and Functionality

Transparency and Regulation: Gold ETFs are regulated by SEBI, offering higher investor protection compared to unregulated digital gold platforms.

Liquidity and Ease of Trade: You can buy or sell units instantly on the stock exchange during trading hours, unlike digital gold, which is confined to platform-specific ecosystems.

No Storage or Insurance Hassles: Since the gold is held in vaults by the fund, you don’t worry about safekeeping or purity.

Tax Efficiency: Gold ETFs are taxed as non-equity mutual funds, and after 36 months, they qualify for long-term capital gains tax with indexation benefits, helping optimize returns.

Tracking Accuracy: Reputed ETFs maintain a low tracking error (typically below 1%), ensuring close alignment with live gold prices.

The Mechanism in Short

When you buy a Gold ETF unit through your broker, the amount is debited from your account, and you receive units in your Demat account. The AMC uses this money to purchase and store gold bullion of equivalent value. When you sell, your units are redeemed at the prevailing gold rate, and the sale proceeds are credited directly to your bank account.

Gold ETFs thus offer a transparent, regulated, and efficient way to participate in gold’s long-term appreciation — without worrying about purity, storage, or resale issues. In the broader debate of Digital Gold vs Gold ETF, ETFs stand out for their strong regulation, liquidity, and suitability for long-term investors seeking portfolio stability and inflation protection.

Digital Gold vs Gold ETF: Key Differences Explained

When it comes to modern gold investment options, both Digital Gold and Gold ETFs allow you to own gold without holding it physically — but they differ greatly in regulation, cost, liquidity, safety, and taxation. Understanding these differences helps you choose the right form of investment for your goals.

Below is a detailed comparison between Digital Gold vs Gold ETF, followed by a clear explanation of which one suits different types of investors in 2025.

Digital Gold vs Gold ETF – Detailed Comparison (2025)

| Feature | Digital Gold | Gold ETF |

|---|---|---|

| Nature of Investment | Direct ownership of physical gold stored in partner vaults | Mutual fund units that represent gold held by the fund |

| Regulation | Not regulated by SEBI or RBI; fully offered by private players | Fully regulated by SEBI under mutual fund guidelines |

| Minimum Investment | As low as ₹10–₹100 | Price of 1 ETF unit (~1 gram of gold, around ₹6,000–₹7,000 as of 2025) |

| Storage & Security | Stored by partner custodians (MMTC-PAMP, Augmont, SafeGold) | Stored by AMCs in RBI-approved and SEBI-monitored vaults |

| Liquidity | Can be sold only on the same platform; depends on platform availability | Can be traded instantly during market hours on NSE/BSE |

| Price Tracking | Based on spot gold price + platform spread & charges | Based on international gold prices with minimal tracking error |

| Purity | 24K (999) guaranteed by platform | 99.5% purity maintained by the fund |

| Costs / Fees | High — 3% GST + platform fees + spread (approx. ₹5 cost on ₹100 invested) | Very Low — ~0.30% expense ratio + brokerage + 0.015% stamp duty (approx. ₹0.40 cost on ₹100 invested) |

| Taxation | Treated as physical gold — STCG taxed as per slab; LTCG @ 20% with indexation after 3 years | Taxed like debt mutual funds (post April 2023) — STCG & LTCG both taxed as per income slab (no indexation) |

| Delivery Option | Can be converted into coins/bars (additional charges apply) | No physical delivery; settled in cash |

| Regulatory Safety | Platform-dependent; no central authority for complaint resolution | SEBI-regulated, with trustees & custodians for investor protection |

| Suitability | Suitable only for micro-ticket buying or gifting; not ideal for short-term or long-term investing due to cost and no regulation | Best for short-term, medium-term, and long-term investing; suitable for SIPs, portfolios, and wealth building |

Which Is a Better Investment in 2025 – Digital Gold or Gold ETF?

Choosing between Digital Gold and Gold ETFs depends on cost, safety, regulation, and long-term suitability. When we compare both options objectively, Gold ETFs clearly offer better value, lower charges, and higher investor protection. Here’s why:

1. Gold ETFs Have Much Lower Costs

Digital Gold comes with 3% GST, platform charges, spreads, and delivery fees.

On average, ₹100 invested in Digital Gold may cost you around ₹5 in charges.

Gold ETFs have minimal expenses — an expense ratio of about 0.30%, small brokerage charges, and 0.015% stamp duty, which equals ₹0.40 on ₹100.

This makes Gold ETFs far more cost-efficient, especially for long-term wealth creation.

2. Gold ETFs Are Regulated, Digital Gold Is Not

Digital Gold is not regulated by SEBI or RBI. If something goes wrong — pricing disputes, platform failure, non-delivery — investors have no official authority to file a complaint.

Gold ETFs are fully regulated by SEBI, with strict rules, auditing, and transparency.

Your ETF units are held in a Demat account, providing additional security.

3. Digital Gold Has Higher Risk Even in the Short Term

Many investors assume Digital Gold is good for short-term holding, but lack of regulation makes it risky even for a few months.

Since platform risk is high, short-term investors can face sudden issues if the vendor stops operations or changes policies.

4. Taxation Is Clearer and More Transparent in Gold ETFs

Gold ETFs follow the updated debt-fund taxation system, making them straightforward to understand.

Digital Gold is taxed like physical gold — GST at purchase + capital gains, which increases total cost.

Plus, long-term digital gold attracts 20% tax with indexation, but the initial GST still reduces net returns.

5. Overall Reliability and Transparency Favour Gold ETFs

Gold ETFs offer price transparency, liquidity, and easy buy/sell through Demat.

Digital Gold depends heavily on the platform’s reliability and operational policies.

For most investors — beginners, long-term planners, or even short-term traders — Gold ETFs offer a safer and cleaner experience.