NRI Home Loan vs Normal Home Loan

NRI Home Loan vs Normal Home Loan in India: Key Differences, Eligibility & Benefits

If you are planning to buy a property in India, choosing the right type of home loan is crucial. But did you know that NRI home loans work very differently from normal home loans for resident Indians? The differences are not just in interest rates, but also in loan tenure, repayment rules, documentation, and tax benefits.

In 2025, with stricter RBI guidelines and rising property demand from overseas Indians, banks and housing finance companies in India have introduced tailored home loan products for NRIs. Understanding how an NRI home loan vs normal home loan compares will help you save money, avoid delays, and make the right financial decision.

In this guide, we explain the exact differences between NRI home loans and normal home loans with a quick comparison table, updated eligibility norms, repayment rules, and expert tips to choose the best option.

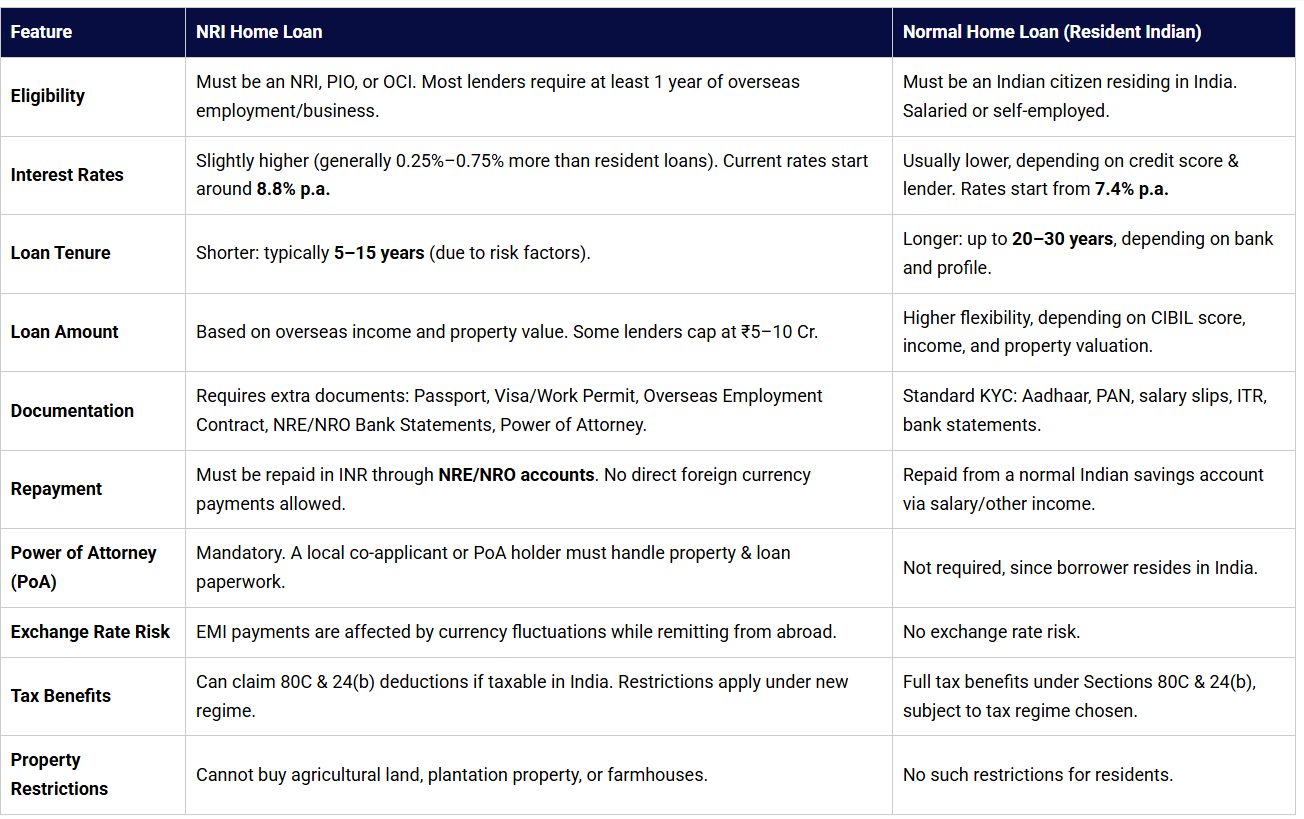

Quick Comparison Table: NRI Home Loan vs Normal Home Loan

| Feature | NRI Home Loan | Normal Home Loan (Resident Indian) |

|---|---|---|

| Eligibility | Must be an NRI, PIO, or OCI. Most lenders require at least 1 year of overseas employment/business. | Must be an Indian citizen residing in India. Salaried or self-employed. |

| Interest Rates | Slightly higher (generally 0.25%–0.75% more than resident loans). Current rates start around 8.8% p.a. | Usually lower, depending on credit score & lender. Rates start from 7.4% p.a. |

| Loan Tenure | Shorter: typically 5–15 years (due to risk factors). | Longer: up to 20–30 years, depending on bank and profile. |

| Loan Amount | Based on overseas income and property value. Some lenders cap at ₹5–10 Cr. | Higher flexibility, depending on CIBIL score, income, and property valuation. |

| Documentation | Requires extra documents: Passport, Visa/Work Permit, Overseas Employment Contract, NRE/NRO Bank Statements, Power of Attorney. | Standard KYC: Aadhaar, PAN, salary slips, ITR, bank statements. |

| Repayment | Must be repaid in INR through NRE/NRO accounts. No direct foreign currency payments allowed. | Repaid from a normal Indian savings account via salary/other income. |

| Power of Attorney (PoA) | Mandatory. A local co-applicant or PoA holder must handle property & loan paperwork. | Not required, since borrower resides in India. |

| Exchange Rate Risk | EMI payments are affected by currency fluctuations while remitting from abroad. | No exchange rate risk. |

| Tax Benefits | Can claim 80C & 24(b) deductions if taxable in India. Restrictions apply under new regime. | Full tax benefits under Sections 80C & 24(b), subject to tax regime chosen. |

| Property Restrictions | Cannot buy agricultural land, plantation property, or farmhouses. | No such restrictions for residents. |

Eligibility:

NRI Home Loan: Must be an NRI, PIO, or OCI. Most lenders require at least 1 year of overseas employment/business.

Normal Home Loan: Must be an Indian citizen residing in India. Salaried or self-employed.

Interest Rates:

NRI Home Loan: Slightly higher (0.25%–0.75% more than resident loans). Current rates start around 8.8% p.a.

Normal Home Loan: Usually lower. Rates start from 7.4% p.a. depending on credit score and lender.

Loan Tenure:

NRI Home Loan: Shorter, typically 5–15 years.

Normal Home Loan: Longer, up to 20–30 years depending on bank and profile.

Loan Amount:

NRI Home Loan: Based on overseas income and property value. Some lenders cap at ₹5–10 Cr.

Normal Home Loan: Higher flexibility depending on CIBIL score, income, and property valuation.

Documentation:

NRI Home Loan: Requires Passport, Visa/Work Permit, Overseas Employment Contract, NRE/NRO Bank Statements, Power of Attorney.

Normal Home Loan: Standard KYC: Aadhaar, PAN, salary slips, ITR, bank statements.

Repayment:

NRI Home Loan: Must be repaid in INR through NRE/NRO accounts. No direct foreign currency payments allowed.

Normal Home Loan: Repaid from a standard Indian savings account via salary or other income.

Power of Attorney (PoA):

NRI Home Loan: Mandatory; a local co-applicant or PoA holder must handle paperwork.

Normal Home Loan: Not required.

Exchange Rate Risk:

NRI Home Loan: EMIs are affected by currency fluctuations while remitting from abroad.

Normal Home Loan: No exchange rate risk.

Tax Benefits:

NRI Home Loan: Can claim 80C & 24(b) deductions if taxable in India; restrictions under the new regime.

Normal Home Loan: Full tax benefits under Sections 80C & 24(b), subject to tax regime chosen.

Property Restrictions:

NRI Home Loan: Cannot buy agricultural land, plantation property, or farmhouses.

Normal Home Loan: No such restrictions.

What is an NRI Home Loan?

An NRI home loan is a special type of housing loan designed for Non-Resident Indians (NRIs), Persons of Indian Origin (PIOs), and Overseas Citizens of India (OCIs) who want to buy, build, or renovate residential property in India.

Unlike normal home loans for resident Indians, an NRI home loan comes with stricter eligibility rules, a shorter repayment period, and additional documentation requirements. In 2025, Indian lenders like HDFC, SBI, Kotak, and ICICI are actively promoting NRI-specific home loan products, especially for those working in the Middle East, the US, UK, and Singapore.

Eligibility for NRI Home Loan (2025)

To qualify for an NRI home loan, borrowers generally need to meet the following:

Residency status: Must be an NRI, PIO, or OCI.

Minimum overseas work experience: Most banks require at least 1 year of employment abroad. For self-employed NRIs, a minimum of 2–3 years of stable business income may be required.

Age: Usually between 21 and 60 years (sometimes 65, depending on lender).

Income criteria: Assessed on foreign salary or business income. Income in stable currencies (USD, GBP, EUR, AED, SGD) is preferred.

Credit profile: Good CIBIL score in India is still important, even if your main income is abroad.

Key Features of NRI Home Loans

Purpose: Purchase, construction, or renovation of residential property.

Tenure: Generally capped at 15 years.

Processing: Requires a Power of Attorney (PoA) in India to handle documentation.

Repayment: EMIs must be paid in Indian Rupees via NRE/NRO accounts. Direct remittance from foreign accounts is not permitted.

Restrictions: NRIs cannot purchase agricultural land, farmhouses, or plantation property.

Like normal home loans, NRI loans also require legal verification of property documents, and in many cases, lenders execute a MOD in home loan (Memorandum of Deposit of Title Deed) as security against the property.

What is a Normal Home Loan?

A normal home loan is the standard housing finance product offered to resident Indians who want to buy, build, or renovate property in India. It is the most common type of loan offered by Indian banks and housing finance companies and is typically easier to access compared to an NRI home loan.

Unlike NRI loans, normal home loans are designed for salaried and self-employed individuals living in India, with longer repayment periods, lower interest rates, and simpler documentation requirements.

Eligibility for Normal Home Loan (2025)

Banks and housing finance companies in India usually set the following criteria:

Residency status: Must be an Indian citizen residing in India.

Age: Typically between 21 and 65 years.

Employment: Salaried individuals (private, government, PSU) or self-employed professionals/business owners.

Income criteria: Based on monthly/annual income in India. Lenders check the debt-to-income ratio to ensure repayment ability.

Credit history: A good CIBIL score (750+) increases eligibility and lowers interest rates.

Key Features of Normal Home Loans

Interest Rates: Usually lower than NRI loans, starting around 7.4% p.a. in 2025.

Tenure: Flexible, going up to 20–30 years, making EMIs more affordable.

Loan Amount: Based on income, repayment capacity, and property value.

Documentation: Simple, with standard KYC (PAN, Aadhaar, income proof, bank statements, property documents).

Repayment: Monthly EMIs through the borrower’s Indian savings account.

Tax Benefits: Residents can claim deductions under Section 80C (principal repayment) and Section 24(b) (interest repayment).

Why Normal Home Loans Are Popular

For Indian residents, normal home loans are more affordable, flexible, and accessible. With longer tenure and lower rates, they allow buyers to plan property purchases without putting extra financial stress. Additionally, the availability of tax benefits makes them a smart financial decision for most households.

Key Differences Between NRI Home Loan and Normal Home Loan

For Indian residents, normal home loans are more affordable, flexible, and accessible. With longer tenure and lower rates, they allow buyers to plan property purchases without putting extra financial stress. Additionally, the availability of tax benefits makes them a smart financial decision for most households.

Eligibility Criteria

NRI Home Loan: Only available to Non-Resident Indians (NRIs), Persons of Indian Origin (PIOs), and Overseas Citizens of India (OCIs). Lenders usually require proof of at least one year of overseas employment or business.

Normal Home Loan: Available to any Indian resident who meets income and credit score requirements. Salaried, self-employed, and business owners are all eligible.

Key Point: NRIs face stricter rules and need to prove overseas income, while residents have a simpler approval process.

Documentation Requirements

NRI Home Loan: Requires additional documents such as Passport, Visa/Work Permit, Overseas Employment Contract, and NRE/NRO account statements. Lenders also ask for a Power of Attorney (PoA) in India.

Normal Home Loan: Only standard KYC documents are needed—PAN, Aadhaar, income proof, property papers, and bank statements.

Key Point: NRIs face more paperwork, while residents enjoy faster and simpler processing.

Interest Rates & Loan Tenure

NRI Home Loan: Interest rates are typically 0.25%–0.75% higher than resident loans. Loan tenure is shorter, usually capped at 15 years, due to risk and compliance rules.

Normal Home Loan: Interest rates start lower, around 7.4% p.a., with a tenure of up to 30 years, making EMIs more affordable.

Key Point: If you need a long-term, low-cost loan, resident loans are more flexible.

Repayment Rules

NRI Home Loan: Repayment must be made in Indian Rupees through NRE/NRO accounts. Direct foreign currency transfers are not permitted.

Normal Home Loan: Repayment is done via EMIs from a regular savings account in India.

Key Point: NRIs must manage forex conversion risks and remittance rules, while residents have a straightforward EMI process.

Property Restrictions

NRI Home Loan: NRIs cannot purchase agricultural land, plantation property, or farmhouses.

Normal Home Loan: Indian residents face no such restrictions.

Key Point: NRIs must limit their purchase to residential or commercial property only.

Power of Attorney (PoA) Requirement

NRI Home Loan: Most banks mandate a local Power of Attorney holder to handle paperwork, property registration, and legal formalities on behalf of the NRI.

Normal Home Loan: Not required, as borrowers can directly complete formalities.

Key Point: This adds an extra legal step for NRIs, making loan processing slightly longer.

Exchange Rate Impact

NRI Home Loan: Monthly EMIs are indirectly affected by currency fluctuations. For example, if the INR weakens against the USD, the NRI may need to remit a higher amount from abroad to cover the same EMI.

Normal Home Loan: No such risk exists, as repayment is fully in Indian Rupees.

Key Point: Exchange rate risk is unique to NRIs and can increase financial burden.

Tax Benefits

NRI Home Loan: Eligible for tax deductions under Section 80C (principal repayment) and Section 24(b) (interest), but only if the NRI has taxable income in India. The new tax regime (2025) restricts these benefits.

Normal Home Loan: Residents can claim the same tax benefits, subject to regime chosen, making it an attractive financial option.

Key Point: Tax deductions are slightly easier to claim for resident borrowers.

Which One Should You Choose? (NRI vs Normal Home Loan)

The choice between an NRI home loan and a normal home loan depends mainly on your residency status and income source. If you are living and earning abroad, you must apply for an NRI home loan—this allows you to invest in Indian property but comes with higher interest rates, shorter tenure, stricter documentation, and repayment through NRE/NRO accounts. On the other hand, if you live and earn in India, a normal home loan is the better option, offering lower rates, longer tenure (up to 30 years), simpler paperwork, and full tax benefits. For NRIs planning to return permanently, shifting to a normal home loan may be possible once residency status changes. In short, overseas earners should go for NRI loans, while Indian residents benefit more from normal home loans.

Need Expert Guidance